How to Improve Your Credit Score Before Applying for a Loan

Applying for a loan is an exciting step, whether you're buying a car, renovating your home, or purchasing your first property. Before you apply, it's worth checking your credit score, as it plays an important role in how lenders assess your application.

The good news is that a few simple changes can help improve your credit profile and strengthen your chances of approval.

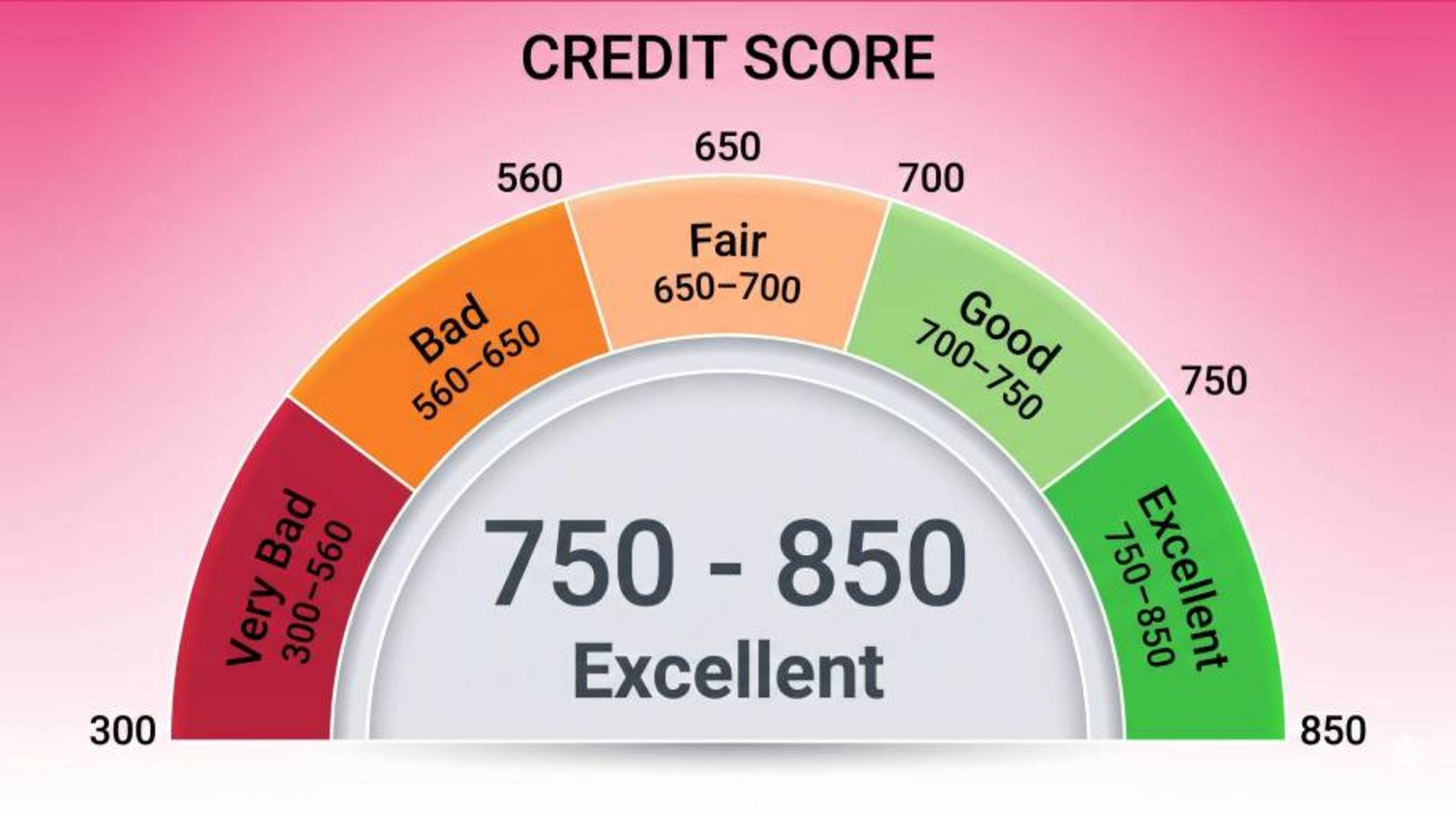

What Is a Credit Score?

A credit score is a numerical representation of your creditworthiness. It helps lenders understand how you've managed credit and financial obligations in the past.

In Australia, credit reporting bodies such as Equifax and Experian collect information about your financial behaviour and use it to calculate a score.

Your credit report may include:

- Repayment history

- Credit cards and personal loans

- Credit limits

- Loan applications

- Defaults or court judgments

- Bankruptcy records

Lenders often use this information alongside your income, expenses, employment, and overall financial position when assessing a loan application.

Why Does Your Credit Score Matter?

A higher credit score can indicate that you've managed debt responsibly over time.

This may help:

- Improve your chances of loan approval

- Access a wider range of lenders

- Secure more competitive interest rates

- Demonstrate financial reliability

A lower score doesn't necessarily mean you'll be declined, but it may limit your options or require additional assessment.

How to Improve Your Credit Score Before Applying for a Loan

1. Check Your Credit Report for Errors

One of the simplest ways to improve your credit score is to review your credit report carefully.

Mistakes can happen. Incorrect defaults, duplicated accounts, or outdated information may negatively impact your score.

Look for:

- Incorrect personal details

- Accounts that do not belong to you

- Incorrect repayment records

- Paid debts still listed as outstanding

If you find an error, contact the credit reporting agency and request an investigation.

2. Pay Bills and Loan Repayments on Time

Payment history is one of the most important factors affecting your credit score.

Late payments can remain on your credit report and may signal higher risk to lenders.

Consider:

- Setting up automatic payments

- Using calendar reminders

- Paying at least the minimum repayment by the due date

Consistent on-time payments can help strengthen your credit profile over time.

3. Reduce Existing Debt

High levels of debt can impact how lenders assess your borrowing capacity.

Focus on reducing balances where possible, particularly:

- Credit cards

- Personal loans

- Buy Now Pay Later accounts

Lower debt levels can improve your overall financial position and demonstrate responsible credit management.

4. Avoid Applying for Multiple Loans

Every credit application may be recorded on your credit report.

Submitting multiple applications in a short period can create the impression that you're experiencing financial stress.

Before applying:

- Research your options carefully

- Check eligibility requirements

- Speak with a broker about suitable lenders

This can help reduce unnecessary credit enquiries.

5. Lower Your Credit Card Limits

Many borrowers are surprised to learn that lenders often consider available credit limits, not just outstanding balances.

For example, if you have a credit card with a $15,000 limit but only use $2,000, lenders may still assess your potential access to the full amount.

Reducing unused credit limits can sometimes improve your lending profile.

How Long Does It Take to Improve a Credit Score?

There is no fixed timeline.

Some improvements, such as correcting reporting errors, can have an immediate impact. Other factors, including repayment history and debt reduction, may take several months to influence your credit profile.

Generally, the earlier you start preparing before applying for a loan, the better.

What Can Hurt Your Credit Score?

Several factors can negatively affect your credit score, including:

- Missing repayment deadlines

- Defaulting on debts

- Multiple credit applications

- High credit card balances

- Bankruptcy or insolvency events

- Unpaid utility or phone bills

Understanding these risks can help you avoid unnecessary damage to your credit profile.

Pull Quote: "Your credit score reflects financial habits over time, not just a single decision."

How a Broker Can Help

Understanding your credit score is only one piece of the puzzle.

A mortgage or finance broker can help you:

- Understand your borrowing position

- Identify potential issues before applying

- Compare lender requirements

- Explore suitable loan options

At Pink Loans, we work with borrowers from a wide range of financial backgrounds and help simplify the lending process so you can move forward with confidence.

FAQs

Can I get a loan with a low credit score?

Yes, some lenders may consider borrowers with lower credit scores. However, available loan options, interest rates, and lending criteria may differ. A broker can help identify lenders that may be suitable for your circumstances.

How often should I check my credit report?

Checking your credit report at least once a year is a good habit. It's also wise to review it before applying for a loan to ensure all information is accurate and up to date.

Does checking my own credit score affect it?

No. Accessing your own credit report or credit score is generally considered a soft enquiry and does not negatively impact your score.

Will paying off debt improve my credit score?

Reducing debt can improve your overall financial profile and may positively influence your credit score over time. Consistent repayments and lower outstanding balances are generally viewed favourably by lenders.

How many credit applications are too many?

There is no specific number, but multiple applications within a short period can raise concerns for lenders. It's usually better to research your options carefully before submitting applications.